9 / 75

9 / 75

8

TOWARDS AMETA THEORY OFACCOUNTING FOR KNOWLEDGE MANAGEMENT: REVIEW THE

REALITIES TO STAGE THE CRITICAL THINKING OF KNOWLEDGE BUSINESS MODEL

SBE, Vol.20, No.1, 2017

ISSN 1818-1228

©Copyright 2017/College of Business and Economics,

Qatar University

success. These new rules have entailed

businesses to fundamentally rethink their past

assumptions about management. Stewart 2007

argues that to understand the unique rules of

knowledge economy especially how to create

value, it is essential to identify the role of three

assumptions. The first is knowledge and its

management as the most important engine of

production. The second is knowledge capital

as a key pillar of the organizational capitals.

The third is how to adopt new knowledge

technologies, business practices, management

techniques and strategies. Gorey

et al

., 1996

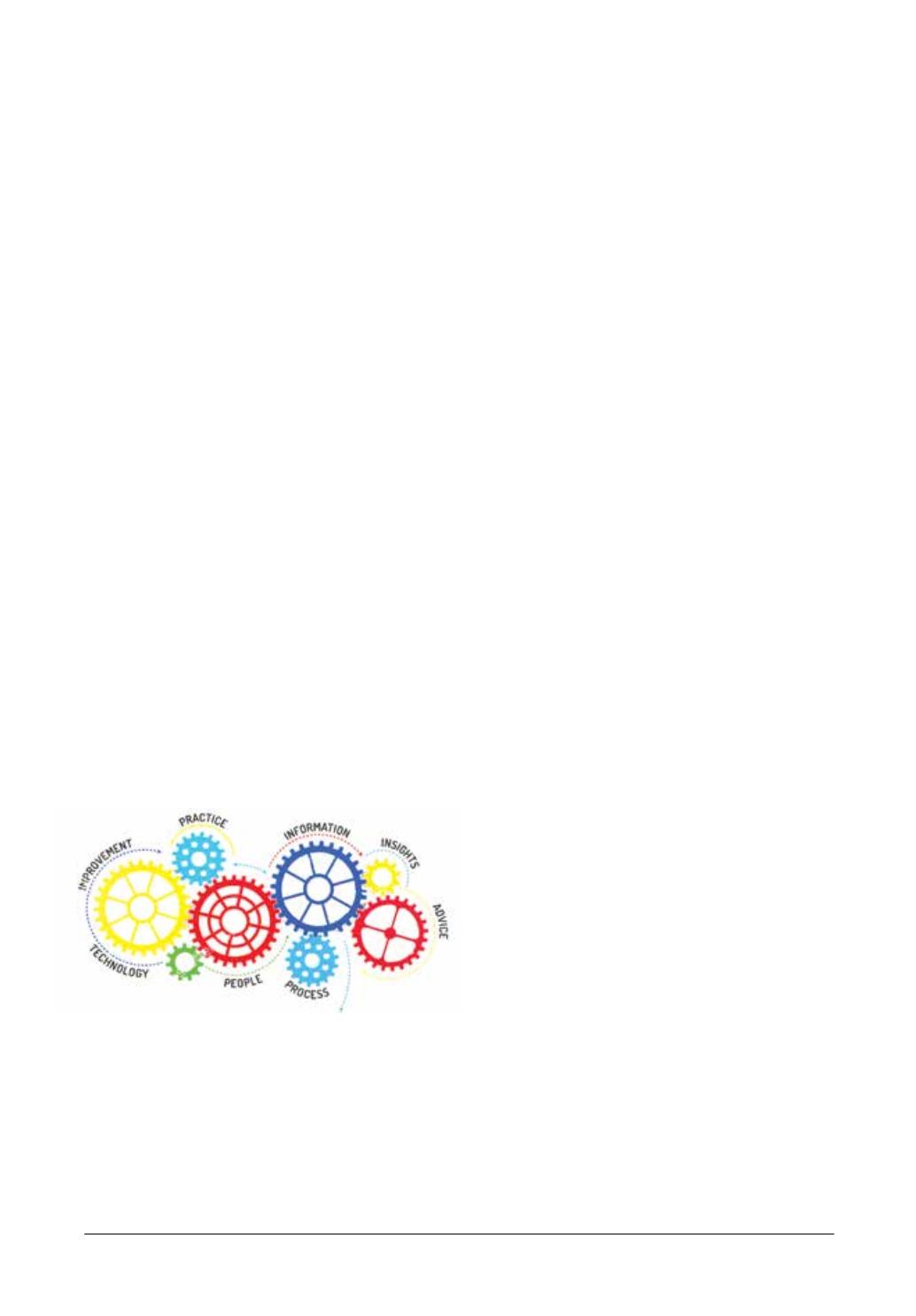

proclaimed that there are four organizational

enablers facilitate the management of the

organizational knowledge. These enablers

are leadership, culture, technology, and

measurement (See Figure-1). The accounting

measurement

is the process that

includes

not only how the organization quantifies its

knowledge capital, but also how resources

are allocated to fuel its growth. Further, it’s

the connection process where accounting

match knowledge management. This unique

relationship has been depicted in Figure-1

below. Knowledge management has improved

profitability by raising productivity and

streamlining, downsizing, outsourcing, andout-

competing the competition (Kurzynski, 2009).

Changing profit patterns and mechanisms has

been considered one of the most fundamental

changes due to the new practices of knowledge

management. These practices are the engine

to translating creative thinking, new ideas,

and innovation into valuable products and

services to guarantee business survive. Value

is the product of knowledge and companies

cannot generate profits without these ideas,

skills, and talent of people. The literatures

especially knowledge oriented contextualize

much of those knowledge strategies, models,

and knowledge-profit relationship (Nonaka

and Takeuchi, 1995; Kaplan and Norton,

1996; Edvinsson and Malone, 1997; Anderson,

2000; Prusak, 2001; Stewart, 2001; Amidon,

2003; Omotayo, 2015). However, beside it is

concentrated on intangibles; the knowledge

management is just as much about people,

organizational processes, and information

technology. It’s more concerned with the

flows of knowledge that take place as part

of organizational processes rather than the

stocks of knowledge presented in financial

reports (Edwards

et al

., 2004). For example,

Nonaka and Takeuchi (1995), link knowledge

management to the organizational success, and

then making profit. They claim that knowledge

companies are profitable because of their

skills and expertise about how to translate

the organizational knowledge into products

and services. This dynamic represents the

virtuous cycle of competition, invention,

innovation, productivity, and growth.

Further, such dynamic cycle combines three

streams: value stream, revenue stream and

the logistical stream. These streams entail that

the knowledge business model has to address:

investment and how it is funded, the ongoing

costs, and the revenue and how it generated

(Mohammad, 2013a). This conceals the fact

that the organizational processes of knowledge

management which center the knowledge

business model have two and only two goals:

to innovate and to market. All of their other

processes are cost. Thus, any knowledge

company to properly function in the knowledge

era, it needs knowledge management

Figure-1: Knowledge Management Arena

(Royalty Image)