18 / 75

18 / 75

Ahmed Ali Mohammad

17

SBE, Vol.20, No.1, 2017

ISSN 1818-1228

©Copyright 2017/College of Business and Economics,

Qatar University

of accounting also identified that the routine

regulating mechanism of accounting needs

radical restructuring-more than updating the

measurement techniques (Howell, 2008). The

dysfunctionality of these components was the

key problem against accounting for knowledge

initiatives. Thereafter, these transactional

components have been analyzed and matched

with necessities of knowledge management

to examine the theoretical and practical

validity of these components. The second

step has investigated the whole side effects

of all the above problems especially the gap

between accounting and market capitalization.

Thereafter, the radical research methodology

of this paper has been designed as more widely

accepted approach to structure a newaccounting

theory against knowledge management. The

typology of the research methods has been

designed carefully to integrate all the literature

trends whether in accounting, business or

knowledge management. The practical

solutions developed identify the criteria for

solving these lacks and paradoxes that need

to be reported. The knowledge management‘s

literatures determines the format of the

information required, its nature, its scope, and

the accounting rules that need to be applied

.

The proposed format of financial statements

may help to draw a milestone in the way of

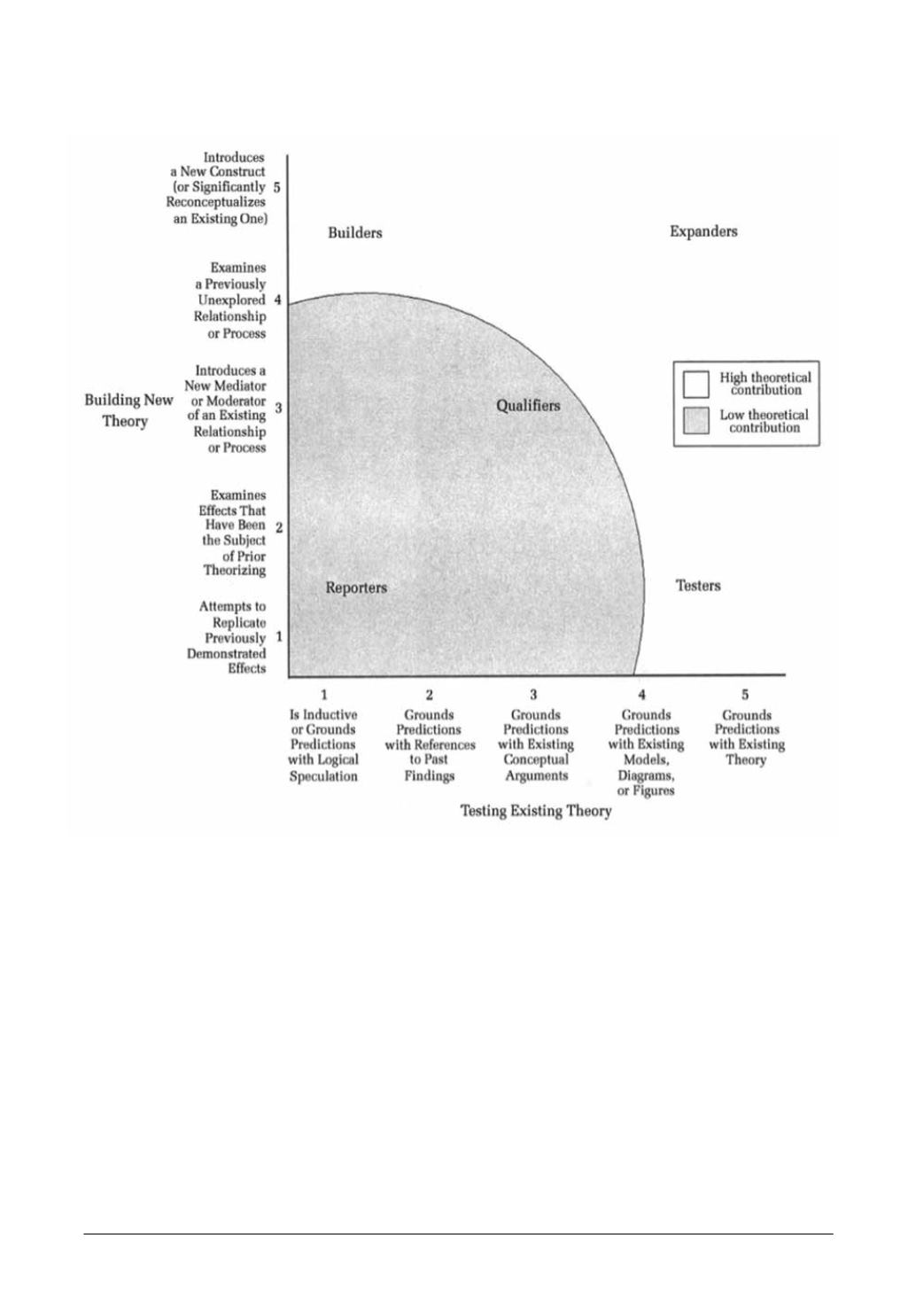

Figure-2: A Taxonomy of the Theoretical Conceptualization

(Source: Colquitt and Zapata-Phelan, 2007)